JCT Estimates Record $1.6 Trillion in Tax Breaks in 2017

The Joint Committee on Taxation (JCT) released a new estimate earlier this year for the cost of tax expenditures over the years 2016-2020. In total, tax expenditures will cost nearly $1.6 trillion in 2017 – the highest in history. That total represents nearly 80 percent of corporate and individual income tax revenue.

The 2017 total is also $130 billion more than the JCT projected for this year in its last report in 2015. The 2015 tax extenders bill – which extended and even made permanent multiple tax provisions – explains approximately five-sixths of JCT’s upward revision for 2017.

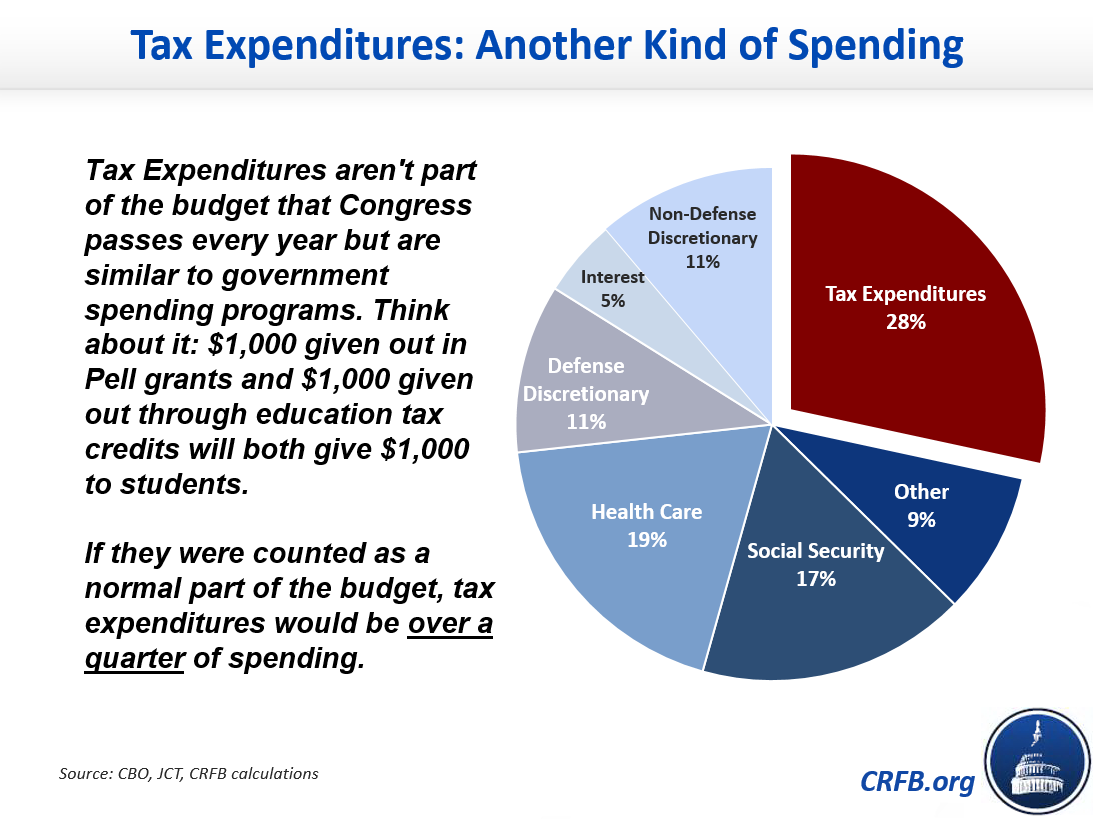

Tax expenditures are sometimes referred to as "spending through the tax code," since they are often functionally equivalent to government spending programs but are not formally included in the federal budget. Tax expenditures would also take up 28 percent of the budget if they were counted as spending – more than every other major budget category.

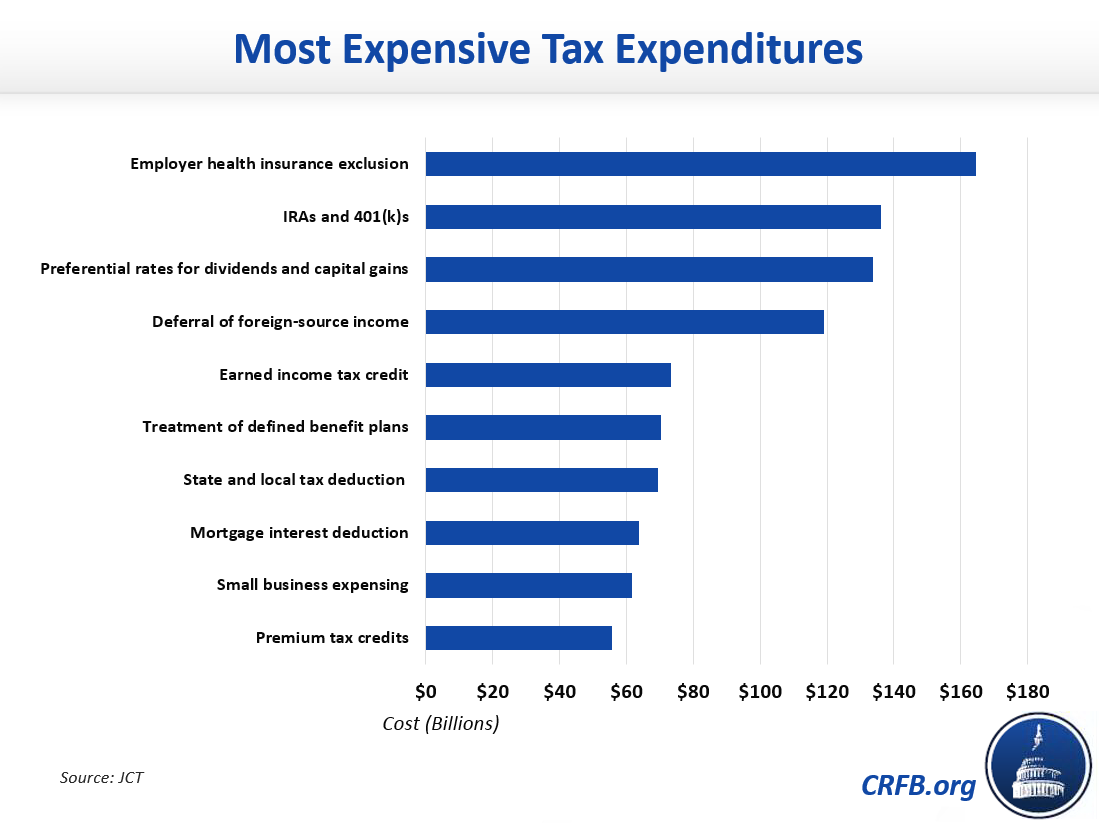

Contrary to popular assumptions, the largest tax expenditures are a handful of widely-used and popular tax breaks – not a few unpopular loopholes like carried interest or preferences for corporate jets.

The employer-sponsored health insurance exclusion is the biggest tax break in the code, representing $165 billion in income tax revenue lost in 2017. This break allows health insurance provided by employers to be a tax-free form of compensation. It also affects payroll tax revenues, and the Treasury Department estimates that the total exclusion costs $2.9 trillion in lost income tax revenue over 10 years (or $4.7 trillion in both income and payroll tax revenue). House Republicans recently were considering, but eventually abandoned, a plan that would have reformed this large tax break.

Other large breaks include the preferential rates for dividends and capital gains, the mortgage interest deduction, and treatment of retirement plans.

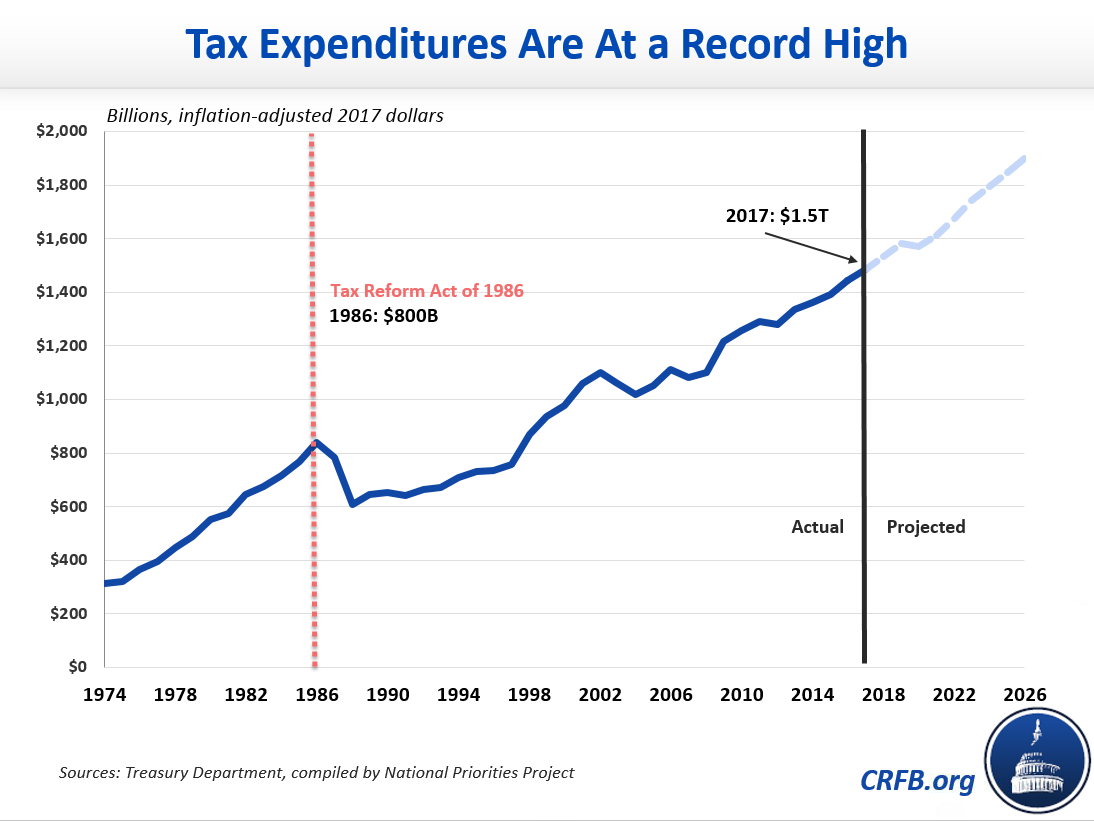

The size and number of tax expenditures, which include various deductions, credits, exclusion, and other exemptions, has grown over time. The current total is roughly double the figure from 1986, the last time when the tax code was overhauled, after adjusting for inflation. The total is also roughly $80 billion higher than the $1.5 trillion that the Treasury Department estimates tax expenditures will lose in 2017. (Treasury uses different methodology and estimates a slightly different set of tax expenditures than JCT does.)

The $1.6 trillion annual revenue loss from tax expenditures calculated by the JCT suggest an area that is ripe for reform. Many of these breaks complicate the code, distort decision-making, pick winners and losers, and tend to be regressive.

Reducing or reforming tax expenditures has the potential to allow comprehensive tax reform to broaden the tax base, lower the rates, grow the economy, and reduce deficits. And it offers a way to make sure tax reform is fully paid for without the use of gimmicks, fuzzy math, or unrealistic growth forecasts.

Tags

What's Next

-

Image

-

Image

-