Discretionary Spending and the Sequester in the Final Budget Conference

The budget resolution conference agreement has passed both the House and Senate. While we previously wrote about the conference's deficit reduction and budget process issues, a likely flash point between Congress and the President will be how the Congressional budget handles discretionary spending and the sequester. While the budget resolution does not call for changes in the discretionary spending limits set under sequestration, the discretionary spending levels in the budget directly and indirectly deviate from the Budget Control Act (BCA).

The conference agreement does this by cutting both non-defense discretionary (NDD) spending below sequester levels and using Overseas Contingency Operations (OCO) funding to allow the defense budget to go above the sequester levels. For FY 2016, the conference agreement would keep spending at the levels set by the sequester. In addition the conference agreement leaves open a mechanism for sequester replacement in a fiscally responsible way, though this may still lead to conflicts between the House, Senate, and White House.

Discretionary spending in FY 2016

For the FY 2016 appropriations season, which we will continue to update on The Bottom Line as bills develop, the agreement abides by the sequester levels for non-war spending, although it would also effectively raise defense spending by creating a $38 billion slush fund in war spending. In effect, this takes the congressional budget to the total defense request in the President's budget, which instead provided sequester relief through the normal defense channel offset with other savings. The President’s budget also provided NDD funding above the sequester with offsets.

Discretionary spending in 2017-2025

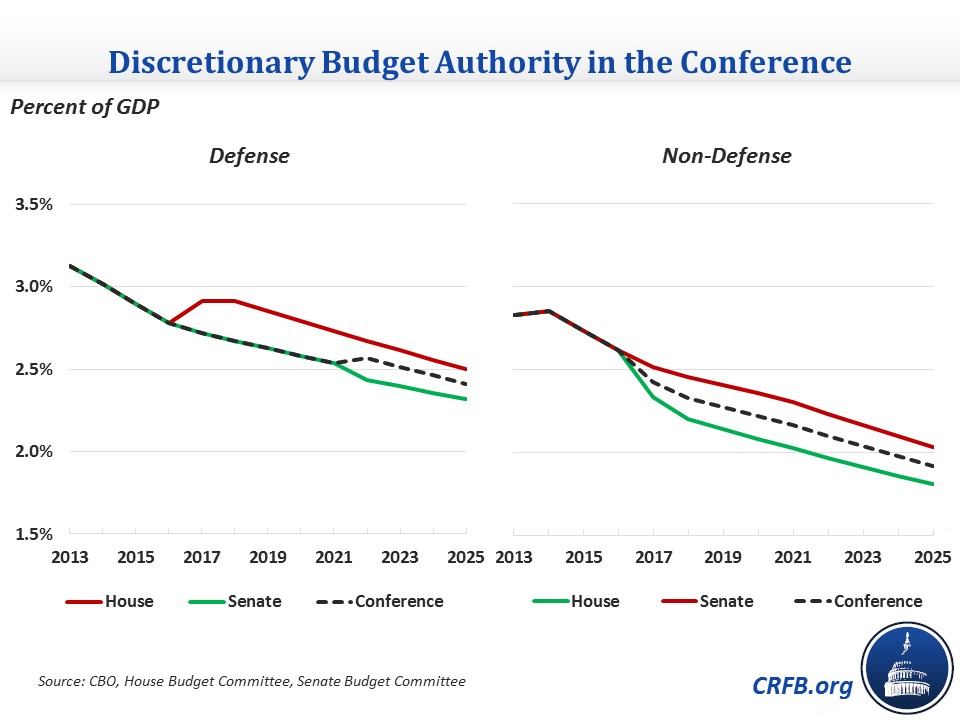

The budget cuts NDD below the sequester by $205 billion from 2017-2021. After 2021, when the sequester and BCA caps expire, the budget is set below the CBO baseline by an additional $291 billion for a total of nearly $500 billion of NDD cuts. There are some further technical cuts in NDD in the budget as a result of the provisions to control CHIMPs to the extent the savings from existing CHIMPs are “baked into” the cap levels. As we explained in our blog "Sharpening the Axe: How the House and Senate Budgets Handle the Sequester," the original House budget had cuts totaling $759 billion in NDD over ten years versus the Senate’s $236 billion, so the conference agreement just about splits the difference.

The conferenced budget does not provide defense sequester relief through 2021 as the House budget did. Defense discretionary spending in the congressional budget is at the BCA sequester levels through 2021, preventing the budget from violating Senate rules. After 2021 and the expiration of the BCA, defense spending is higher than CBO’s baseline levels.

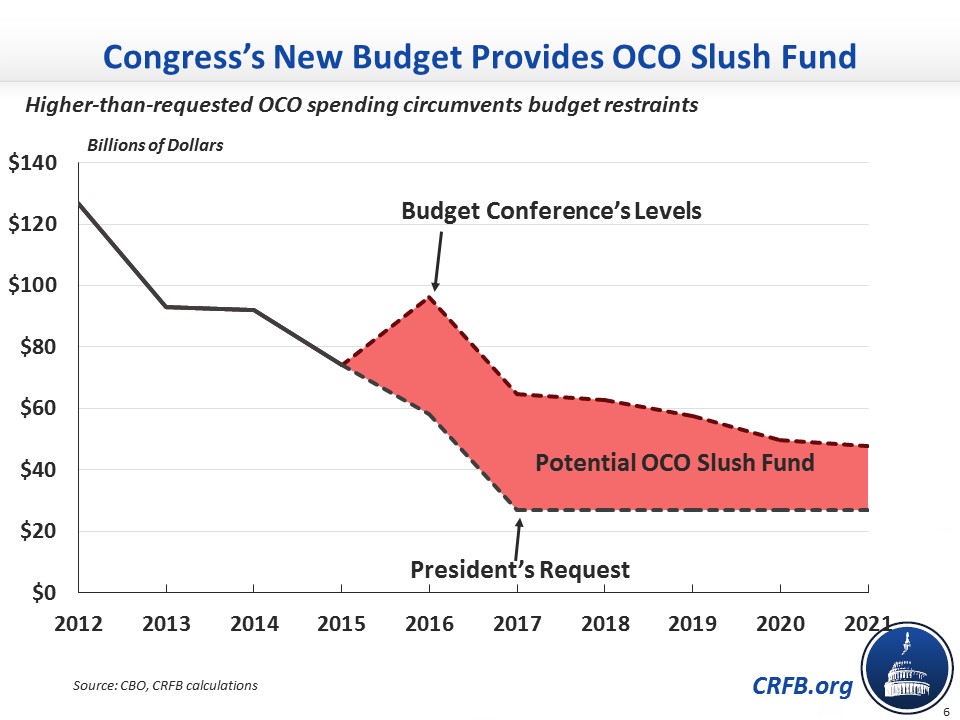

However, as we have written many times, the budget provides a significant slush fund to get around the BCA caps through the OCO designation. Total OCO budget authority is $187 billion higher than the President’s request and $190 billion higher than CBO’s war drawdown scenario. The higher OCO spending creates a bridge to the higher defense spending provided after the expiration of the caps in 2021, making it clear that OCO is being used for backdoor sequester relief.

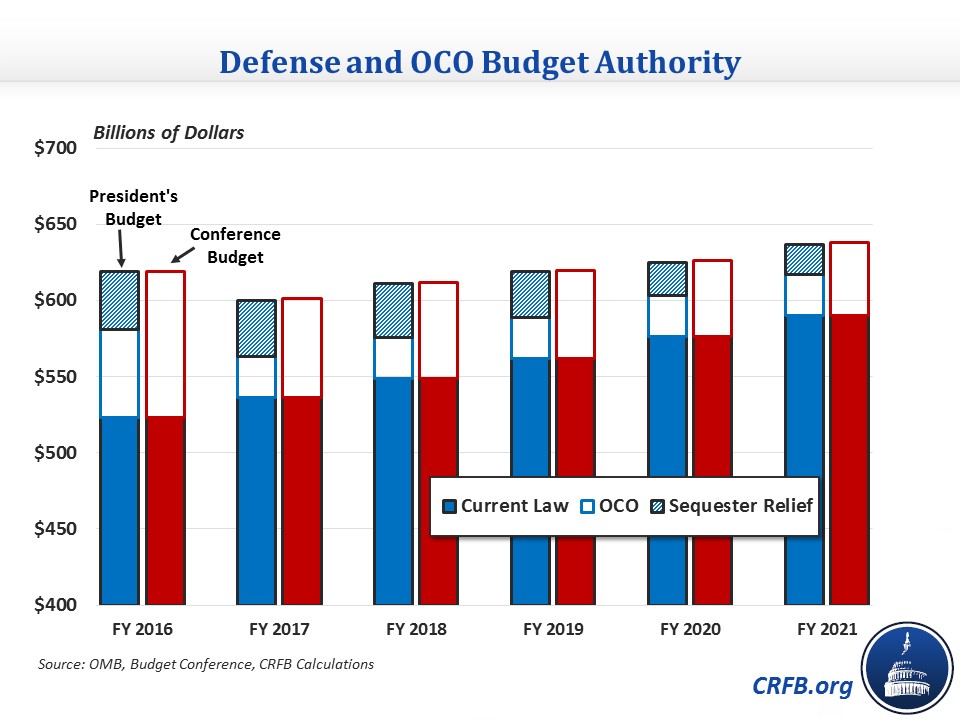

In fact, the combined defense-OCO spending levels in the budget resolution are almost identical to the President’s each year despite the fact the budget resolution includes no direct sequester relief while the President does. In other words, the budget resolution is calling for the exact same defense sequester relief as the President, but using additional OCO spending to finance it through 2021 to avoid responsibly offsetting the costs. This will likely create conflict near the end of the fiscal year because the President has threatened to veto appropriations bills which use OCO for non-war items. After 2021, the President's and the congressional budgets provide nearly the same increased defense spending.

Opportunities for sequester relief

The conferenced budget contains a deficit-neutral reserve fund (DNRF) for the Senate that allows defense and non-defense discretionary spending to be increased above the limits if offset by other savings in the budget. While it doesn’t require sequester relief be split evenly between defense and non-defense or explicitly say that offsets should come from tax expenditures and spending cuts as the Senate budget did after adoption of the Kaine amendment, the DNRF has the flexibility to provide sequester relief to Defense and/or NDD and allows offsets to be spending cuts or revenues. The House budget had a DNRF allowing increased defense discretionary spending if offset by spending cuts only.

****

All of these differences potentially set up a showdown in the fall over sequester relief between the House’s position limiting sequester relief to defense spending offset by other spending cuts and the Senate position allowing sequester relief for both NDD and defense discretionary and allowing revenues as well as spending cuts to offset it. But more importantly, it sets up a conflict between Congress and the President over how much sequester relief to provide and in what way. The conferenced budget's emphasis on providing sequester relief only on the defense side has already drawn a veto threat from the White House because it does not include any sequester relief for NDD.

For all of our writing on the budget conference and the FY 2016 budget season see our blog.